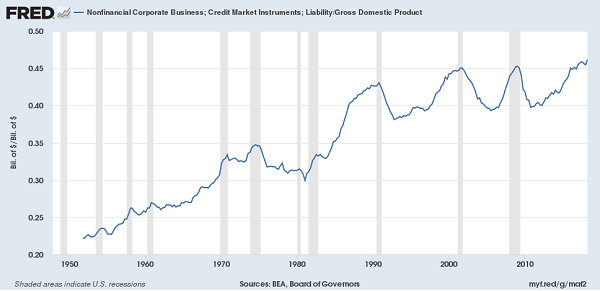

Nonfinancial corporate debt to GDP has reached its highest post-war level as per first chart below. Although corporate leverage is expected to rise in expansionary years, its elevated level tends to be a leading indicator for increases in credit risk, as well as systemic risk according to the last three recessions.

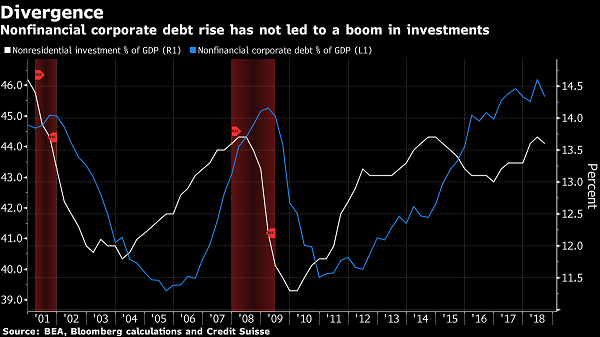

Furthermore, in contrast to previous cycles, this increase in leverage has not been associated with an increase in investments. The second chart below depicts non-residential investment which has been bouncing between 13 and 13.5% since 2012. Thus, instead of borrowing to invest in productivity capacity companies may have been using their debt for stock buybacks and other ways to extract cash for shareholders.

There are two additional risk indicators that should be of concern. First, the majority of new issuance of investment grade bonds has been at the BBB grade. According to the Office of Financial Research, BBB-rated issuance was a record 56% of all U.S. investment-grade issuance during the 12 months ending September 2018, well above levels before the financial crisis. A downgrade for a significant portion of these bonds could cause a liquidity crunch with ripple effects. Second, leveraged lending has rapidly grown over the last few years to $1 trillion, which represents more than 11% of nonfinancial debt and a record high.

At the same time, the slope of the treasury yield curve (10yr-3m), one of our favourite leading economic indicators, is pointing towards a recession in the next 18-24 months.

Banks have been experiencing relatively low delinquency rate in their C&I portfolio, as depicted in the chart below. Given the current risk repricing in credit and equity markets, C-suite and board members may be wondering how the above could affect their C&I as well as CRE and consumer credit portfolios due to contagion.

As banks plan ahead for expected losses (CECL ALLL) and unexpected losses (Capital), they should be using macroeconomic scenarios that capture the above forward-looking paths of the economy with the appropriate likelihood of occurrence in order to quantify the impact of such scenarios on their porfolios. Banks that proactively do so now will weather the next recession the best.