The Board of Governors of the Federal Reserve System (FRB), the Federal Deposit Insurance Corporation (FDIC), the National Credit Union Administration (NCUA), and the Office of the Comptroller of the Currency (OCC) have recently updated the FAQs for CECL.

It is worth noting that the new FAQs, listed in the Appendix, deal with an approach that some banks may have followed for selecting their macroeconomic scenarios and consequentially their reasonable and supportable (R&S) horizon for CECL by piggybacking on the DFAST/CCAR scenarios.

As we have shown elsewhere, the selection of the scenario and duration of the R&S horizon is critical for the accuracy and procyclicality of the expected lifetime loss estimation and hence allowances of a bank.

Thus, the agencies state that the DFAST/CCAR methodology, scenarios and models are meant for stress testing purposes. Banks should not automatically select nine quarters as the R&S horizon just because this is the horizon of the CCAR scenarios. Banks should provide reasonable and supportable evidence for the selection of the R&S horizon independently of their stress testing process. The R&S horizon should not be set arbitrarily, without evaluating its impact on the lifetime loss.

The agencies also state that the CCAR scenarios including the baseline scenario should not be considered as forecasts of the macroeconomic variables and are therefore not meant for CECL forecast purposes.

Furthermore, the agencies point out that the banks should be using “economic variables and other factors relevant to the collectability of an institution’s portfolios”. The keyword in this clause is relevant.

- Are macroeconomic scenarios at the national level relevant to the collectability of a portfolio of a regional/community bank with a specific geographical footprint?

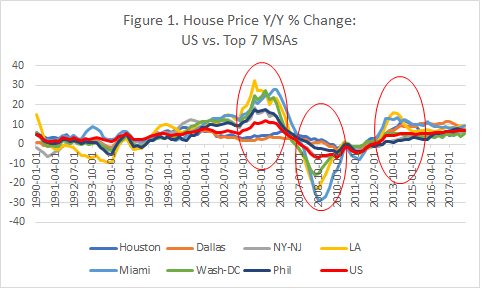

If a bank is using the US price index, shown in red, for forecasting expected credit loss for its residential mortgage portfolio, it may introduce significant inaccuracy and procyclicality in its allowance and hence earnings volatility.

- Are macroeconomic scenarios at the national level relevant to the collectability of a Multifamily CRE portfolio of a bank given the different credit cycles across asset classes and geographies?

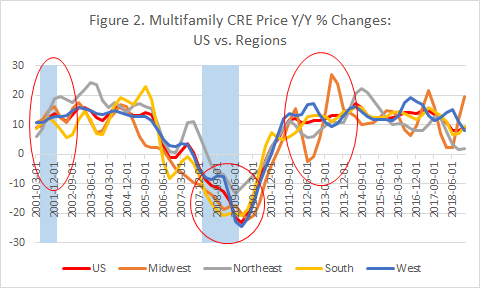

Figure 2 illustrates the difference between the Multifamily CRE cycle vs. the US economic cycle, shown in light blue, and the difference of Multifamily CRE across regions. Although Multifamily CRE was more resilient than other CRE asset classes during the great recession, it experienced a U-type recession in Midwest and South compared to a V-type in the rest of the regions and US. Ignoring these differences may result in significant inaccuracy in allowances and earnings volatility.

- How can a bank combine forecasts of relevant macroeconomic factors for CECL estimation across asset classes and geographies in a coherent way and with a specific likelihood?

For answers to the above please check our white paper.