The Big Six Canadian Banks reported their year-end results last week. Half of them missed expectations following a similar pattern in 2019 Q3. The news in this earnings release though was the significant rise in allowances and provisions for credit losses.

Thus, in this article we analyze:

- possible causes for this rise, and

- lessons learned that can also be useful to the US banks preparing for the CECL standard.

The analysis is based on the IFRS9 disclosures from Canadian Banks and our experience with implementing the standard. These disclosures are similar to the ones the US banks will be providing under CECL. Hence, in addition to their forward-looking nature for risk measurement, the two standards bring more transparency to the banks results and allow a reader to better understand their allowances and provisions.

Before delving into the analysis let us explain the main difference between the two standards: when a loan originates, CECL requires lifetime expected credit losses (ECL) to be recognized whereas IFRS9 requires ECL only for the next 12 months. Past loan origination IFRS9 prescribes a three-stage approach for recognizing credit losses: initially Stage 1 with a 12-month ECL; migration to Stage 2 in the event of significant increase in credit risk (SICR) and calculation of lifetime ECL; migration to Stage 3 when the loan is deemed to be impaired and lifetime ECL also applies. In addition, IFRS9 requires more than one macroeconomic scenario for estimating the ECL, whereas CECL just one. The scenario likelihoods are used as weights in the ECL calculation. Disclosure of the scenario weightings is not required.

- Could changes in the scenarios and weightings this quarter have caused the rise in provisions?

Due to staging, IFRS9 provisions can be more procyclical than CECL. The lower the SICR threshold, the more sensitive the transition from Stage 1 (12 month ECL) to Stage 2 (lifetime ECL), namely the “cliff effect”, and the higher the provisions and the capital deduction are. Disclosure of the SICR threshold(s) is not required by the standard. Although IFRS9 results in lower provisions through the cycle than CECL, the management of the SICR threshold and resulting “cliff effect” can create a lag to recessions (procyclicality) and may therefore challenge institutions substantially more in recessions than CECL.

- Could changes in the SICR threshold(s) combined with the “cliff effect” be explaining part of the rise in provisions?

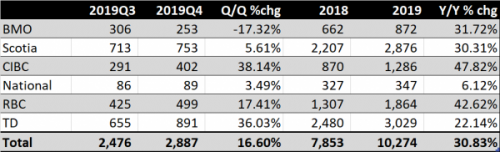

Table 1 presents the Q4 and annual provisions together with the changes from previous quarter and year. The total provisions for credit losses increased by 17% q/q and 31% y/y on average. Table 2 shows the ratio of total provisions to loans. We should point out the y/y increase of the ratio as well as the significant variability of the ratio and its growth across the six banks. The three banks that had double digit growth in the total provisions and ratio from last quarter were the ones that missed earnings expectations.

This underlines how critical provisions can be for the bank’s earnings, and hence why we have been advocating for design choices in the implementation of the two standards that minimize procyclicality and forecasting error (read this procyclicality article for more). Similar variability in the provisions is also expected amongst the big US banks when the CECL standard comes into effect in January 2020 (read this article for more).

Table 1. Total provisions for credit losses from Big 6 Canadian Banks

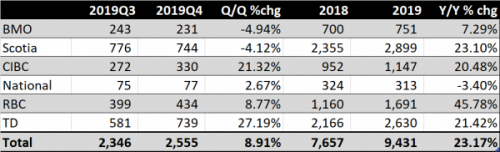

Table 2. Total Provisions for Credit Losses as % of Loans

Q: Is the rise in provisions observed in all three stages of IFRS9?

Tables 3 and 4 break down the total provisions by Stage 3 loans, i.e. impaired, and Stage 1&2 respectively. Table 3 shows that the majority of the rise in total provisions is mainly due to an increase in provisions for impaired loans. Four of the six banks reported a q/q increase and five out of six a y/y increase for Stage 3 provisions. The average increase was 9% q/q and 23% y/y.

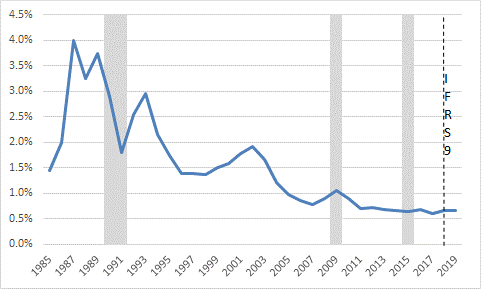

However, the increase in total provisions may not be the biggest story in these results because the total provision ratio is rising from historically low levels. Figures 1 & 2 depict the time-series of the total provision ratio and loss allowance ratio on average for the big six banks. Shaded areas in the two graphs denote the recessions in the Canadian economy. IFRS9 did not have a significant impact on average when it came into effect in January 2018.

Table 4 shows that five out of the six banks reported a much bigger growth (%) for Stage 1&2 provisions than for Stage 3. The average growth was 150% q/q and 328% y/y. Again, there was a lot of variance amongst the banks and the three banks that had an increase in Stage 1&2 provisions from last quarter were the ones that missed expectations. In their earnings reports, the banks justified these increases to changes in the scenarios and migration.

Table 3. Provisions for Stage 3 loans from Big 6 Canadian Banks

Table 4. Provisions for Stage 1&2 loans from Big 6 Canadian Banks

Figure 1. Total Provisions for Credit Losses as % of Loans

Figure 2. Loan Loss Allowance as % of Loans

Q: What might have caused the significant rise in provisions?

We already talked about the increase in Stage 3 provisions. Although the majority of the impaired loans are in Retail (residential mortgages and consumer), the y/y increase is mainly due to the Commercial loans.

The key question for a bank dealing with such increase is what percentage of the Stage 3 loans in Q4 were in Stage 2 in Q3. We strongly recommend this performance statistic for backtesting the effectiveness and predictiveness of the staging mechanism. We have been monitoring and reporting it for our clients.

For example, if a significant percentage of the loans went into Stage 3 without spending any time in Stage 2, the thresholds on PD for SICR, i.e. Stage1-to-Stage2 migration, might have been set rather high. This can amplify the “cliff effect” we discussed above. On the one hand, setting the quantitative criteria too low may create many false positives for significant increase in credit risk, resulting in volatility in provisions. On the other hand, relatively high criteria may mask out significant increases in credit risk, resulting in procyclicality in provisions. Namely, provisions will move in tandem with a downturn, instead of gradually rising few quarters prior to that.

The factors responsible for the growth of Stage 1&2 provisions are not as straightforward. This is due to the number of models and assumptions involved, as well as the non-prescriptive nature of IFRS9, similarly to CECL, that allows institutions to follow different methodologies for risk measurement and overlays.

For this reason, there could be a confluence of factors responsible for the growth of Stage 1&2 provisions rather than a single one for each bank. We next examine each of these possible factors.

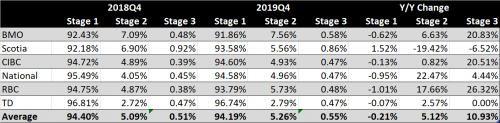

- New business volume. Retail loans are about 68% of total loans on average amongst the Big Six banks, and Business/Government 32%. During 2019, Retail credit grew by about 5% with CIBC having the lowest growth amongst the group at 2%. Business/Government grew by about 15% with TD having the lowest growth at about 9%. In Table 5 we present the breakdown of total loans by IFRS9 Stage and its y/y change. All the banks with the exception of Scotia had a drop in Stage 1 and an increase in Stage 2&3 loans. Scotia exhibited a completely opposite pattern. The three banks with an increase in Stage 1&2 provisions had an increase in total Stage 2 loans, although CIBC and TD had a small one. The increase in Stage 1&2 provisions for the three banks seems to be due to an increase in Stage 2 loans (referred to as “migrations”) rather than an increase in new business volume. The latter would have been classified as Stage 1.

Table 5. Breakdown of Total Loans by IFRS9 Stage

- Change in the macroeconomic scenarios from last year. Since 2018 the banks have been reporting three scenarios for a few key macroeconomic variables. The three scenarios are: baseline, upside and adverse. The variables are Canada Real GDP, Canada Unemployment rate, Canada House Prince Index (HPI) and WTI Oil price. Real GDP and HPI have become slightly more pessimistic in 2019 vs. 2018 on average, WTI more pessimistic, and Unemployment rate slightly less pessimistic. In Table 6 we summarize the baseline and adverse scenarios for HPI for the six banks. Amongst the three banks that reported a big increase in Stage 1&2 provisions, only TD had more pessimistic values (>50%) overall for the scenarios for GDP and HPI compared to last year. CIBC had more pessimistic values for only HPI, and RBC had similar values from last year. Thus, although the revision of the scenarios cannot explain by itself the significant change in Stage 1&2 provisions, it might be one of the contributing factors for the aforementioned credit migrations and higher ECL.

As an aside, we strongly recommend the use of HPI scenarios at a more granular level than national, i.e. at least at the CMA level. Due to changes in regulations and local economies, house prices have evolved significantly differently across Canada over the last 18 months. Ignoring these dynamics in the forward-looking scenarios may increase the error in the risk measurement of Retail portfolios and mortgages in particular, and hence increase procyclicality in provisions and earnings volatility. We also recommend regularly backtesting the forecasting models generating the scenarios.

Table 6. The Baseline and Adverse Scenarios for Canada House Price Index (HPI)

- Change in the likelihood of the scenarios. As mentioned, the scenario likelihoods are used as weightings for calculating the ECL. For example, the baseline, adverse and upside scenarios for 2018 might have been defined with 50%, 15% and 35% likelihood, whereas the likelihoods for 2019 might have changed to 50%, 35% and 15% respectively, in order to reflect potentially higher odds for a recession over the next couple of years. Banks do not disclose the weightings they used. A revision of weightings might have contributed to the increase in Stage 1&2 provisions.

- Increase in 30+ days past due. This state of delinquency is considered as the backstop for migration of loans to Stage 2 even when the SICR criteria are not met. Out of the three banks with a big increase in Stage 1&2 provisions, only TD had a significant increase in 30+ days past due year over year, about 23%. Thus, this result combined with the more pessimistic values in scenarios for GDP and HPI could explain the increase in Stage 1&2 provisions for TD.

- Change in the quantitative criteria for migrations to Stage 2. The criteria for SICR, i.e. Stage1-to-Stage2 migration, are based on absolute and relative thresholds on the expected PD for the remaining life of the loan presently vs. at the time of origination. Some of the banks might have changed the thresholds for the criteria from 2018. Similar to the scenario weightings banks do not disclose these thresholds.

Concluding remarks

- The IFRS9 disclosures can help a reader of the statements better understand the credit risk in the balance sheet of the banks as shown above. We expect this to be the case with the CECL disclosures, which are even more extensive than the IFRS9 ones, going down to the vintage level.

- The “cliff effect”, a feature embedded in IFRS9 but not in CECL, has amplified the significant increase in the allowances and provisions for the Big Six banks for 2019.

- Provisions can be critical for banks’ earnings, hence the need for on-going backtesting of the staging, models and assumptions involved, including the macroeconomic scenarios and their weightings.

- We have only scratched the surface with the above analysis. The question remains whether this increase in provisions is an one-time adjustment or the start of a trend. Stay tuned for further analysis.