One of the criticisms of regulatory stress testing is the assumption of constant balance sheets for banks during the horizon of a stress scenario. In this article we examine some of the recent trends in banks’ balance sheets in order to understand the importance of this assumption.

In its latest semi-annual report on the soundness of the banking system (April 2021), the Federal Reserve Board (FRB) identified three areas of focus given ongoing uncertainties:

- Decline in bank credit growth, particularly when leaving out PPP loans

- Decline in NIMs

- Slight increase in delinquency rates combined with a continuation of loan modifications, particularly in real estate loans and from smaller banks.

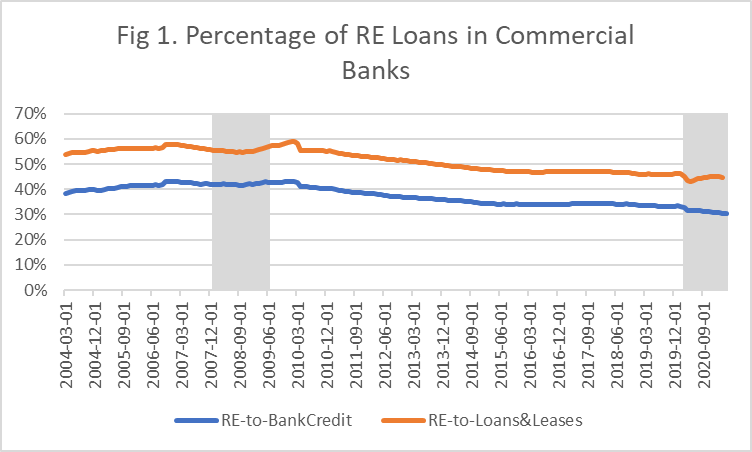

Re. the first area of focus, Figure 1 depicts the monthly time-series (as of April 28) of two ratios for Real Estate (RE) loans for all commercial banks: RE loans to Bank Credit and RE loans to Loans and Leases. The first ratio takes into account potential shift towards securities in bank credit. The second ratio is affected by the growth in PPP loans during the pandemic induced recession. Both ratios are below pre-pandemic levels, with the ratio of RE loans to Bank Credit trending downwards to early 1990’s levels; more on this below.

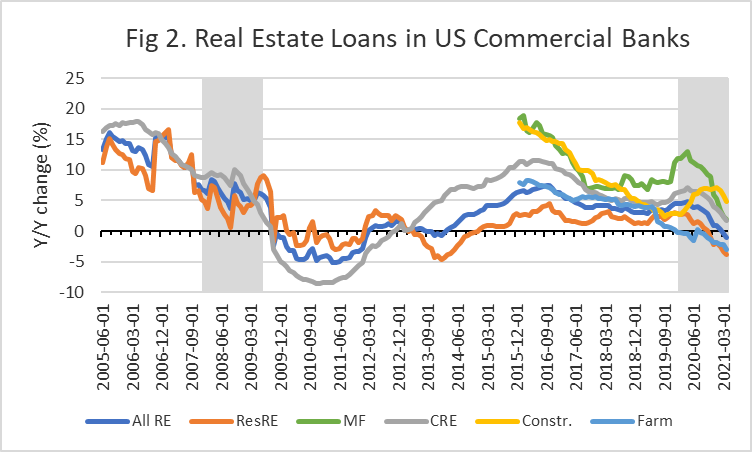

To analyze this negative trend of RE loans during the pandemic we looked at the monthly time-series of the y/y change for each of the RE loan types (H.8 release from FRB). Figure 2 depicts these time-series. Although there has been a decline of credit growth across all RE categories since the second half of 2020, the overall negative growth of RE loans is driven by the negative growth of Residential RE loans. The category of Construction loans is the only RE category that remains higher than pre-pandemic levels.

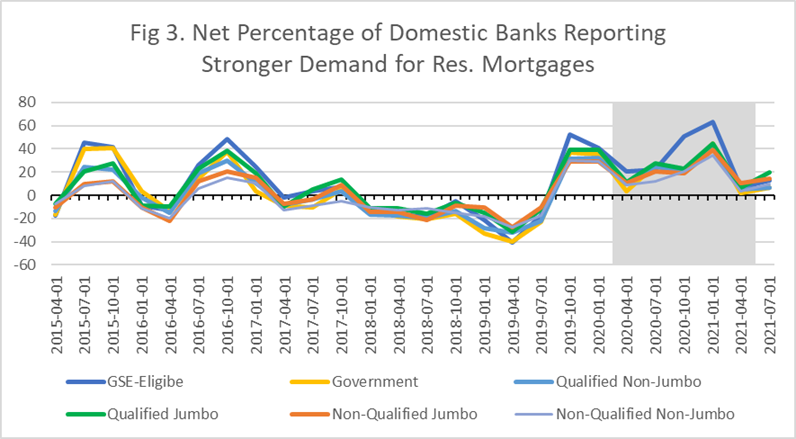

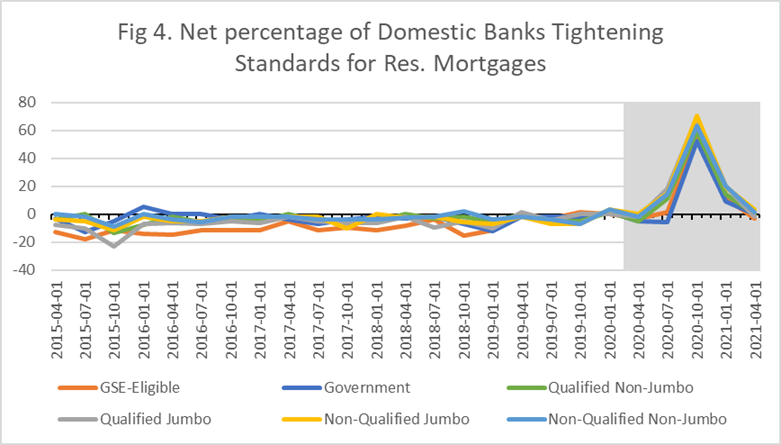

The negative growth of Residential RE loans in particular is striking given the healthy conditions of the residential real estate market. In addition, in the latest Senior Loan Officer Opinion Survey on Bank Lending Practices (FRB, April 2021) banks reported positive demand (Figure 3) and easing standards (Figure 4) for all types of residential mortgage loans. Are banks losing market share in Residential RE to nonbank mortgage lenders?

Re. the second area of focus in the FRB report, the decline in RE credit growth combined with the explosive growth in deposits has resulted in banks investing in lower yielding assets and therefore in a decline in NIMs. Thus, Figure 5 depicts the ratio of Treasury and Agency securities to Bank Credit.

The ratio reached a record level of 26% at the end of April from 21.7% pre-pandemic. This is the highest level since April 1994. Interestingly enough, although the 1990-91 recession ended in the spring of 1991, the mid-1990s was a period where real U.S. home prices continued to fade for years until they bottomed out in 1997.

- Regulatory stress testing is meant to capture the impact on net revenue from stresses in the existing portfolios of banks.

- The above analysis illustrates that the assumption of constant balance sheet in the regulatory stress testing prevents a bank from capturing the impact on net revenue from changes in credit growth and mix. These impacts can be significant as banks have been currently experiencing.

- We therefore recommend that banks also perform stress testing internally, using dynamic balance sheets during the horizon of the stress scenario(s). This is the approach we have been implementing for our clients.