Many US banks have posted higher-than-expected noninterest expense growth in their 4Q21 earnings due to inflationary pressures from wages. For example, Goldman Sachs Group Inc. shelled out an additional $4.4 billion on compensation in 2021, JPMorgan Chase an additional $3.6 billion, and Citigroup Inc. an additional $2.9 billion.

Wage increases and labor shortage are also affecting smaller banks and credit unions according to this recent article on American Banker.

Although wage increases become necessary to handle the increase in prices, they contribute to further price hikes.

Figure 1 shows the median wage growth from the Atlanta Fed’s Wage Growth Tracker. The series is smoothed using a three-month average. The median wage growth has just surpassed the peak level before the Great Recession and is on its way to the record levels of the series in the late ‘90s.

- Have wages set the perpetual inflation machine in motion?

Fig 1. Median Wage Growth (Source: Atlanta Fed)

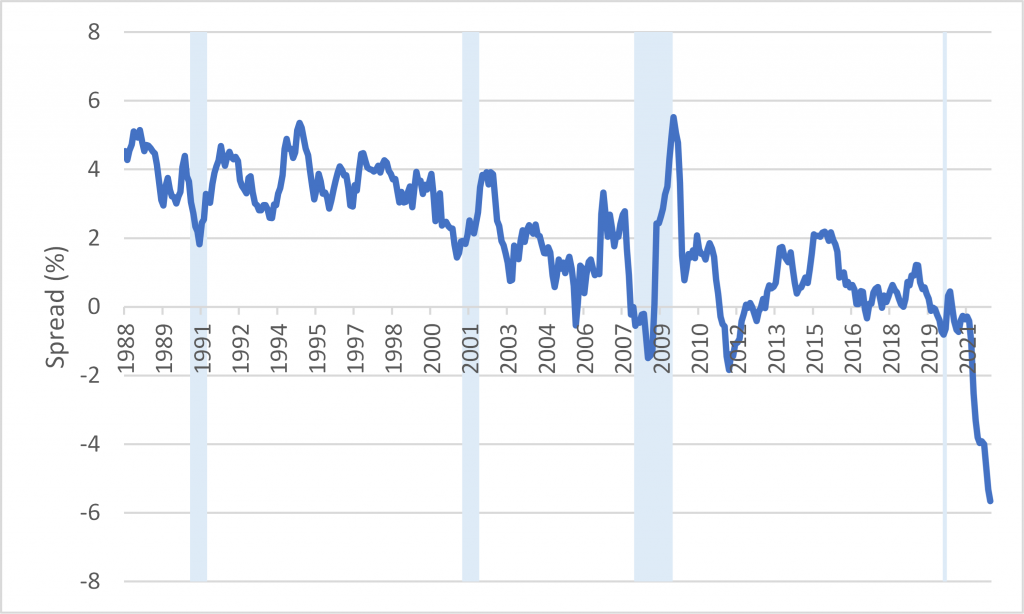

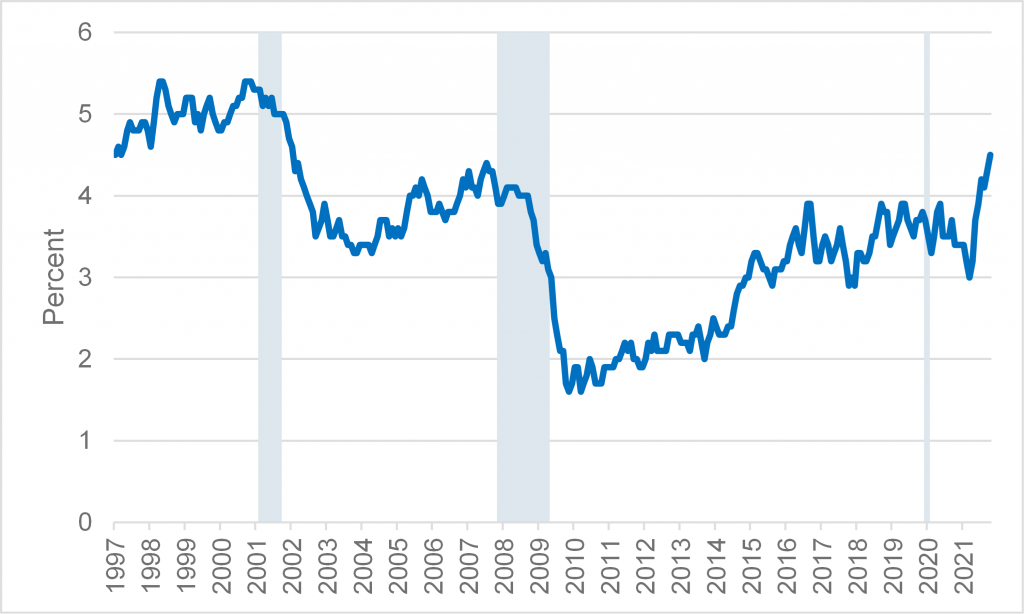

Figure 2 depicts the 10yr-2yr slope of the Treasury yield curve. The Fed Funds rate is shown in Figure 3 and the 10yr-CPI spread in Figure 4.

- Will the Fed be able to raise rates without inverting the yield curve since the latter has already flattened a lot?

- What would this entail for the economy as inversion of the curve typically precedes a recession, see Figure 2?

- How would such scenario impact the bank’s earnings and the credit quality of its assets?

Fig 2. 10yr-2yr Treasury yield spread

Fig 3. Federal Funds Rate

Fig 4. Spread of 10yr Treasury yield – CPI y/y