Macroeconomic forecasts are one of the key drivers of CECL reserves due to the non-linear effects of macro factors on losses. Yet, practitioners tend to focus on the loss quantification technique and assume consensus estimates as the “baseline” macroeconomic scenario for forecasting losses. This approach may satisfy the new standard since the latter only requires one scenario to be used. However, such approach does not consider the uncertainty of the scenario and its impact on the loss estimation.

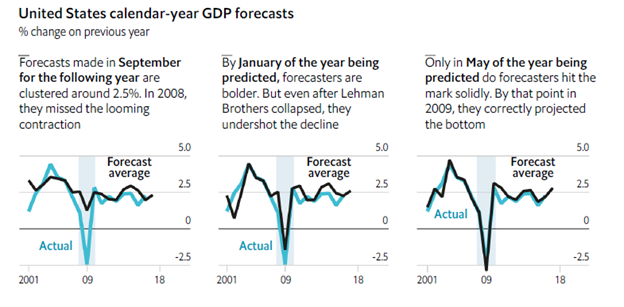

Research has shown that there is a significant lag in consensus forecasts. The Economist (Dec 15 2018) analyzed a database of projections by banks and consultancies for annual GDP growth for various countries. As illustrated in Figure 1 for the case of US, when the economy deteriorates significantly the consensus estimates tend to show slower deterioration and vice versa when it improves. Similar magnitude and tendency of error is also reported in a study by Federal Reserve economists for the FOMC summary of economic projections.

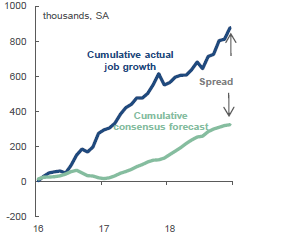

Figure 2 shows the error in consensus forecasts for Employment growth in Canada (Global Economics, Scotiabank). Even during a period of economic expansion consensus has hugely underestimated cumulative job growth.

What would happen to the allowance estimate of your bank if there was a significant error in the macroeconomic forecasts within the “reasonable and supportable” horizon? Wouldn’t this make the bank’s allowances more procyclical, and hence earnings more volatile? How can one select scenario(s) that mitigate this risk in loss estimation in an unbiased way?

For answers to these questions please check our white paper: http://www.infoagora.com/paper/macroscenarios-for-CECL/

Figure 1. Error in consensus forecasts for US GDP (Source: The Economist)

Figure 1. Error in consensus forecasts for US GDP (Source: The Economist)

Figure 2. Error in consensus forecasts for Canada Employment (Source: Scotiabank)