In our previous analysis of the Canadian Banks’ FY2019 provisions we posed the question whether the significant y/y increase in provisions is an one-time adjustment or the start of a trend. In this article we address this question by examining the sensitivity analysis that the banks have provided as part of the IFRS9 ECL disclosures.

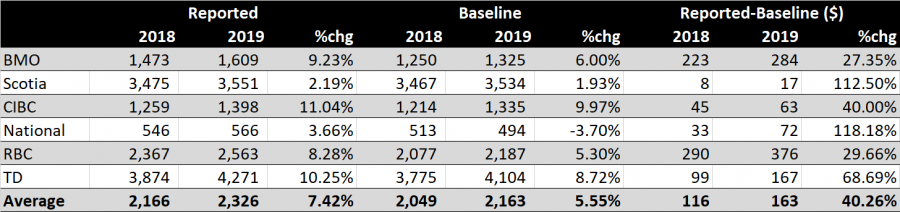

More specifically, in Table 1 we present a y/y comparison of the Reported ACL for Stage 1&2 versus the respective ACL under the Baseline scenario only. As mentioned in our previous analysis, the Big 6 Canadian banks are using 3 scenarios: baseline, upside and adverse. Although different scenario weightings are used for the calculation of ECL across the banks, the baseline scenario is expected to have the biggest weighting compared to the other two scenarios. Thus, since the banks cited the revision of the scenarios as one of the reasons for the increase in allowances and provisions, a comparison of Reported vs. Baseline ACL would provide evidence on whether the scenarios are a reason for the increase.

From Table 1, we observe that the y/y increase in reported ACL for Stage 1&2 is also evident in the baseline ACL, with the exception of National Bank where the baseline ACL dropped y/y by about as much as the reported ACL went up. In fact, National’s baseline scenario for GDP and Unemployment as of October 31 2019 is similar to last year’s baseline scenario, whereas it is more optimistic for HPI. Hence, for National Bank it must have been the other two scenarios and their relative weightings that are offsetting this apparent drop and are resulting in an increase in the reported ACL.

For this reason, Table 1 also shows the spread between Reported and Baseline ACL and the y/y change. Not surprisingly, National Bank has the highest change in the spread at 118%. Scotia has the second highest y/y change in the spread at 113%, even though the spread is the lowest amongst the Big 6 in absolute terms. The remaining three banks exhibit an increase in the spread in the range of 30-70%.

- Does the increase in the Reported-Baseline spread indicate a potentially bigger contribution of the adverse scenario to the overall Stage 1&2 ACL?

- Why does Scotia has the lowest Reported-Baseline spread amongst its peers?

Table 1. Comparison of Reported vs. Baseline Stage 1&2 ACL for Big 6 Canadian Banks

The answer to the first question could depend on a few factors. One would have to take into account an increase in the spread from y/y shifts in the portfolio risk and higher migrations to Stage 2 that could make the portfolios more sensitive to the adverse scenario due to the non-linearities of the loss with respect to macroeconomic variables. As shown in our previous article, National and RBC had significant y/y increase in the Stage 2 migrations.

The increase in the spread could also be due to a change in the weighting of the adverse scenario relative to the other two scenarios for the ECL estimation, or to the adverse scenario becoming more pessimistic than the previous year. The scenario weightings are not disclosed by the banks.

BMO, CIBC and RBC had similar adverse scenarios for the three macroeconomic variables compared to the ones last year. TD, the other bank with an increase in the spread, had more pessimistic values for GDP and HPI in its adverse scenario in 2019 than in 2018. Four of the six banks (BMO, Scotia, CIBC and National) disclose the ACL sensitivity of their adverse scenarios relative to baseline. National had the biggest y/y change in this ACL sensitivity at 8.7% with the other three banks below 1%.

Last but not least the path of the macroeconomic variables under the adverse scenario might have changed its shape, with the trough occurring sooner than previously and therefore having a bigger impact on the ECL. Again we cannot comment on this factor because the above banks have not disclosed such paths for the macroeconomic variables, only their averages for the next 12 months and remaining period.

Hence, based on the available disclosures, the main reasons for the widening of the spread per bank seem to be as follows: RBC due to Stage 2 migrations, National due to Stage 2 migrations and more adverse scenario severity relative to baseline, TD due to more adverse scenario severity. There is not enough information for the reason for the widening of the spread for BMO, Scotia and CIBC.

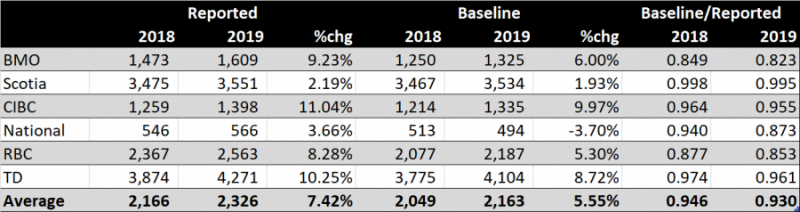

To answer the second question, we present the ratio of Baseline to Reported ACL in Table 2. It is worth noting that Scotia’s ratio is almost 1. This implies that the other two scenarios hardly have any impact on the Stage 1&2 ACL. It could be happening for a number of reasons: a relatively high weighting on the baseline scenario, the adverse scenario not being pessimistic enough to explore the non-linearities of the loss, and/or the underlying ECL models not being capable to capture those non-linear sensitivities. CIBC and TD also exhibit a high ratio of Baseline to Reported ACL, albeit a bit lower at 0.96. Such overreliance on the baseline scenario may become a source of procyclicality in the provisions and earnings volatility if there is a downturn in the economy during the forecast period. In contrast, BMO, RBC and National have a ratio between 0.82-0.87 in 2019, a drop from 0.85-0.94 in 2018. We do not know whether this drop, more significant in the case of National, was achieved by changing the weightings of the scenarios, making the scenarios more pessimistic or a combination of the two. Nevertheless, the less reliance on the baseline scenario, the less procyclical the provisions are going to be.

Table 2. Comparison of Reported vs. Baseline Stage 1&2 ACL for Big 6 Canadian Banks

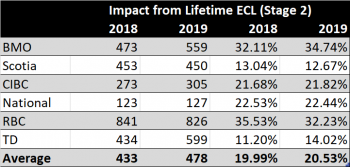

Table 3 presents the impact on the Reported Stage 1&2 ACL from lifetime ECL due to staging, i.e. the so-called “cliff effect”. The effect varies a lot amongst the six banks. It shows how sensitive ECL can become as Stage 2 migrations increase. In contrast, there has been little variation y/y for each bank. It is not clear why the impact for National Bank remained almost the same y/y and it slightly dropped y/y for RBC even though the Stage 2 loans increased y/y for these two banks as per previous article. The variance of Stage 2 migrations amongst banks will be analyzed in a future article.

The “cliff effect” does not exist in the CECL standard for the US banks, making the CECL ECL less procyclical than the IFRS9 one.

Table 3. Impact of Lifetime ECL (staging) on Stage 1&2 ACL for Big 6 Canadian Banks

Concluding remarks

- Our analysis of the Big 6 banks’ disclosures has shown that the increase in the reported Stage 1&2 ACL is arising from an increase in the baseline ACL and widening of the difference between Reported and Baseline Stage 1&2 ACL.

- The severity of the adverse scenario has increased for a few of the banks.

- Although the actual scenario weightings are not known, the baseline scenario is the main driver of the Stage 1&2 ACL. Three out of the six banks seem to be too overweight on the baseline scenario with potential implications for procyclicality.

- Based on points 1-3 and the banks’ disclosures we expect the increase in the Stage 1&2 ACL to continue for the Big Six Canadian banks.

- Furthermore, given the overall increase in Stage 2 migrations, the Stage 3 provisions may increase during the coming quarters. It will depend on the cured rate of the respective Stage 2 loans.

- The above analysis, similarly to the one in our previous article, has pointed out how key assumptions and risk parameters can introduce significant variability in the ECL, over time and amongst peer groups.