As we get ready to welcome 2022, are there any key risk factors which emerged this year and are expected to influence the economy next year?

Inflation and its implication for interest rates are by far the No. 1 risk factor for the economy going into 2022. Following our previous post on inflation, we examine its emergence as a key risk factor and its impact on forecasting economic growth.

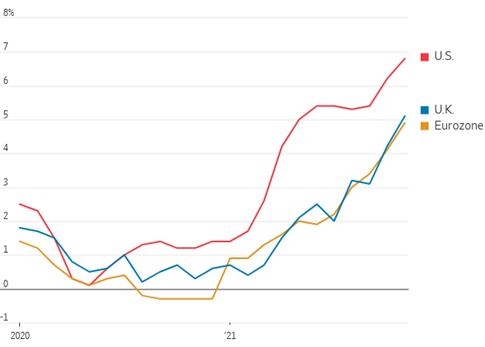

Figure 1 depicts the annual change in CPI for US, UK, and Eurozone. Although rising inflation since the start of this year seems to have been a global trend, it has been much more pronounced in the US. Because of this, central banks are moving towards tightening monetary policy.

Fig 1. Annual change in CPI (Source: Wall Street Journal)

At the same time, the ongoing uncertainty due to the pandemic has forced central banks and mainstream economists to repeatedly revise their outlook for the economy during the year.

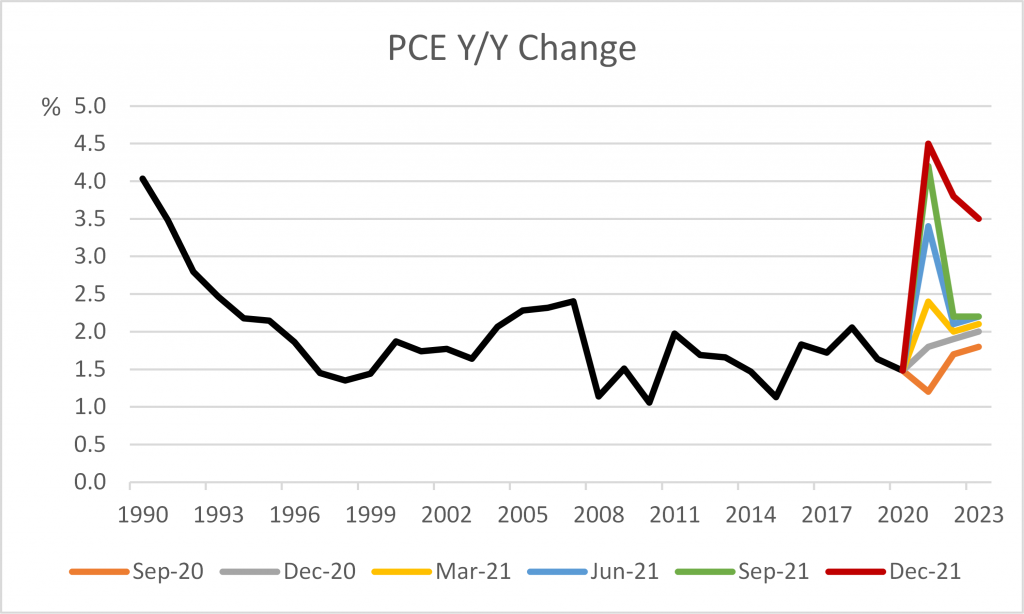

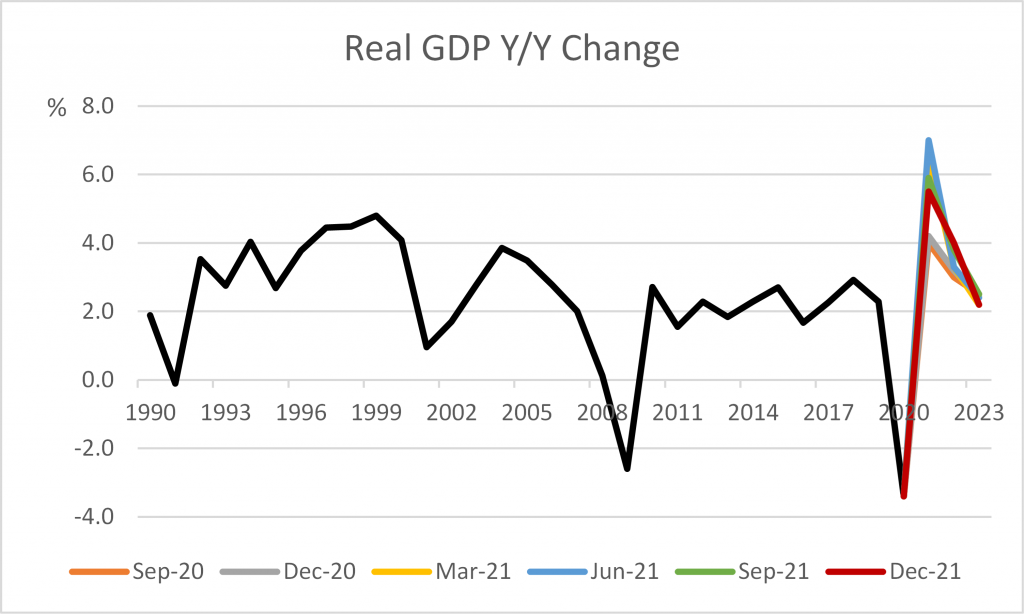

Thus, Figures 2 and 3 show the median projections for US PCE Inflation (excl. food and energy) and GDP from the Federal Open Market Committee (FOMC) meetings between September 2020 and December 2021. The projections are expressed in Y/Y changes.

Within a period of 15 months the median projections for PCE for 2021, 2022 and 2023 were raised by 330, 210 and 170bps respectively. On the other hand, economic growth was revised upwards for 2021 and 2022 by 150 and 100bps respectively, and downwards for 2023 by 30bps.

Due to the significant revision in PCE, the median projections from FOMC of the policy rate for 2022 and 2023 were also raised by 80 and 150bps respectively, as shown in Figure 4.

It is worth pointing out that the median projection for 2023 for the Federal funds rate is at 1.6% and for PCE at 3.5%, whereas in 2018 the Federal funds rate was 2.27% and PCE at 2.1%.

Time will tell whether expectations about inflation will continue to rise and require a tighter monetary policy response from the Fed.

Fig 2. Personal Consumer Expenditures (PCE) excl. food and energy, FOMC median projections

Fig 3. Real GDP, FOMC median projections

Fig 4. Federal funds rate, FOMC median projections

Scenario analysis has become an imperative tool for navigating through uncertainty. Given the above significant revisions in economic forecasts and as the pandemic continues to weigh on the broader economy:

- How often does your financial institution update scenarios (e.g. baseline, stress, etc.) for the specific economy that it operates in?

- How often does your financial institution use the most up to date economic scenarios to review and revise its decision making across use cases, from strategic and business planning to credit origination, credit review, reserving and capital planning?

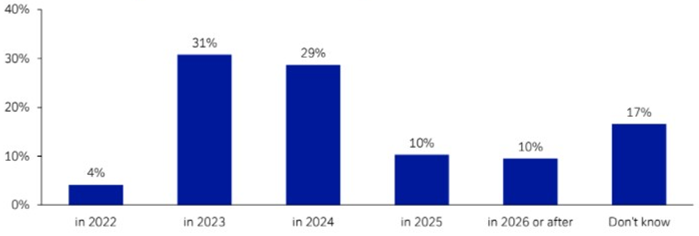

We end this article, our last one for this year, with a survey on when the next US recession will occur. It was conducted by Deutsche Bank Research during December 6-9, 2021, with over 750 responses. They are summarized in Figure 5. 64% of the respondents expect the next US recession to occur by 2024.

Fig 5. Deutsche Bank Research Survey: When will the next US recession occur?

Wishing everyone a safe and healthy New Year!