In a poll we recently conducted at a community bankers’ forum, selection of the forecasting method ranked by far as the top challenge for CECL implementation. Scenario selection was ranked as number two. What is the reason for this feedback?

Due to the non-prescriptive nature of the new standard, FASB has provided a non-exhaustive list of forecasting methods that would be considered compliant. Although adopting any of those methods would tag an implementation as CECL compliant, each of them incorporates different assumptions and complexity/accuracy trade-offs, namely no free lunch.

Let us consider, for example, the methods of static pool loss rate and weighted average remaining maturity (WARM). These methods have gained a lot of interest because of their simplicity and low complexity in implementation. However, they cannot capture changes in loan origination, effects from aging and maturity, and future macroeconomic impact on the collateral[1]. For this reason, in the joint webinar of April 11 from FASB and the six regulatory agencies it was stated that the WARM method is not a regulator preferred or “safe harbor” method.

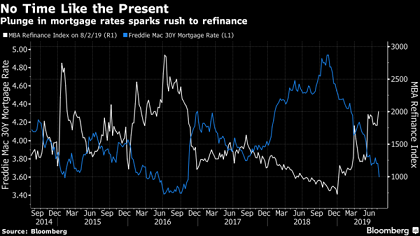

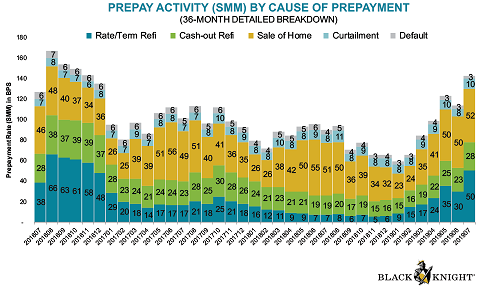

Thus, to estimate the average remaining life of a pool of loans in WARM, one would use an average prepayment rate. Community banks are reported as experiencing an increase in loan payoffs in C&I and CRE loans due to the point in the economic cycle and expectations about future economic conditions[2]. Moreover, the significant decline in mortgage rates has given rise to a jump in refinance activity as reported by MBA and Black Knight, in Figures 1 & 2 respectively. As seen from Figure 2, in July 2019 overall prepayments were up over 60% from a year ago, with rate/term refinances up almost seven times. Furthermore, the vintage of 2018 is the one driving those refinances, prepaying at an 80% higher rate than other vintages. There is also a difference in prepayment rates across states.

Figure 1. MBA Refinance Index

Figure 2. Breakdown of prepayment activity

The challenge from increased loan payoffs and refinances that banks are currently facing underlines the importance of having a loss estimation method which can forecast the expected life of a loan and prepayments as a function of the economic and market environment. Of course, a bank could opt to account for this effect through a Q-factor adjustment, but at the expense of potential inaccuracy in the expected loss estimate and negative consequences on earnings volatility and profitability.

In fact, from our experience with backtesting alternative forecasting methods, the error in the loss forecast can be up to 3 times. Even in cases where a bank has to resort to Call Report data due to insufficient internal data, there are methods with better performance and less limiting assumptions than the WARM method.

- How can a bank select the appropriate loss forecast method for each of its portfolios?

- How can a bank select macroeconomic scenarios relevant to the collectability of each portfolio?

For help with the above questions please contact us.

contact@infoagora.com

(416) 877-1965 | (646) 380-1883

[1] Please read our white paper on CECL procyclicality for further analysis of the WARM method.

[2] https://www.americanbanker.com/news/smaller-banks-fear-customer-flight-as-loan-payoffs-spike